Traditional banks have long dominated the financial services industry, facilitating transactions between individuals and organizations. However, a new trend has emerged: embedded finance. This allows non-financial companies to seamlessly integrate financial services directly into their offerings.

This shift is significantly impacting the global banking landscape. A 2022 Accenture survey analysis predicts that embedded finance could generate up to $92 billion in additional revenue for banks by 2025. Similarly, a Bain & Company report estimates the embedded finance market in the US alone could surpass a staggering $7 trillion by 2026.

Embedded finance is revolutionizing the financial services industry in 2024, offering unprecedented opportunities for both traditional players and new entrants. This trend is driven by the seamless integration of financial services into non-financial platforms, creating a more convenient and user-friendly experience for consumers.

Key Characteristics of Embedded Finance in 2024

- Convenience: Imagine booking a flight and securing travel insurance within the same app or buying a product online and receiving instant financing at checkout. Embedded finance eliminates the need to switch between apps or platforms to access financial services.

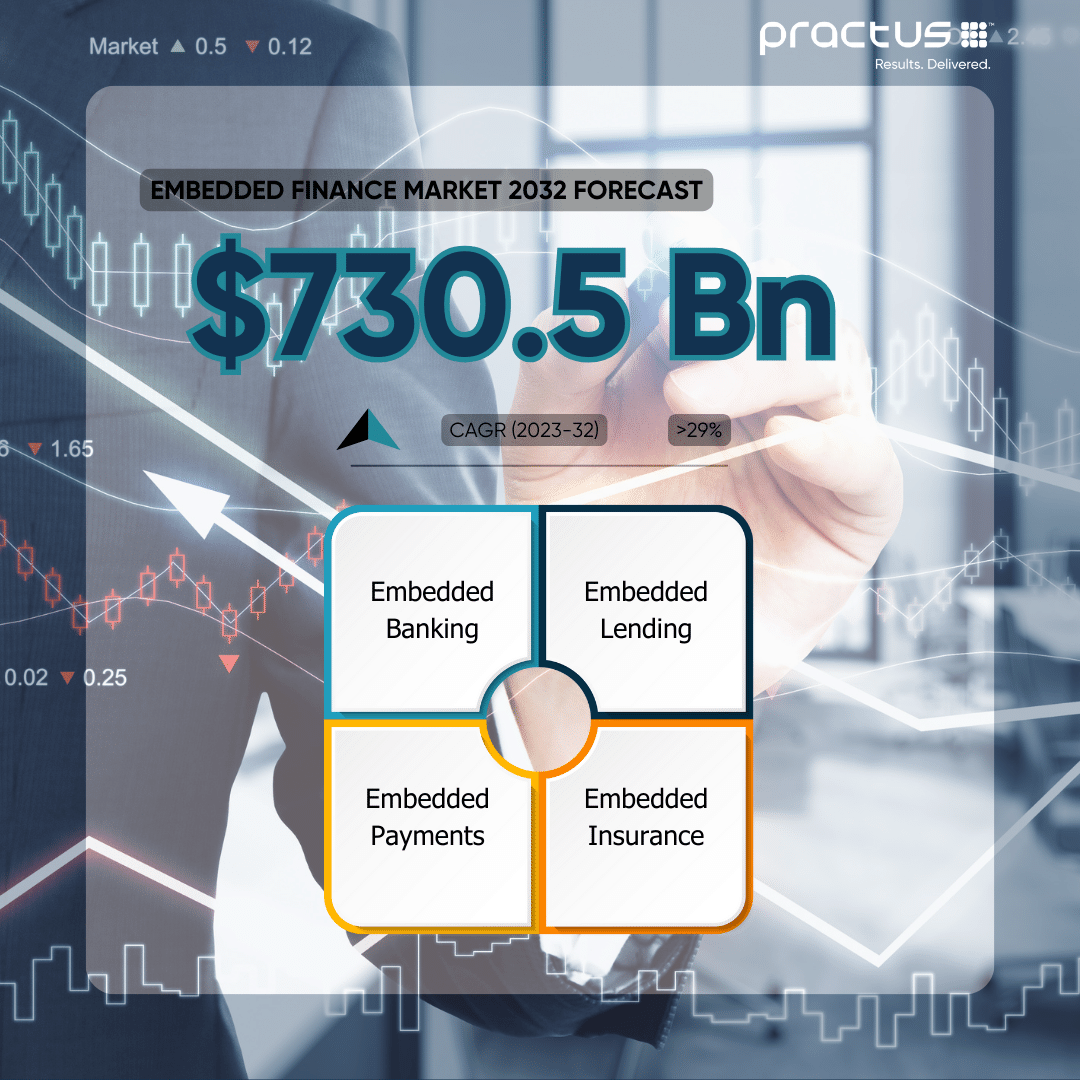

- Growth Potential: Industry experts predict a significant rise in the embedded finance market, with estimates reaching $7.2 trillion for embedded banking services within the next decade.

- Focus on User Experience: Embedded finance personalizes the financial experience by tailoring services to fit the specific platform and user base.

- Collaboration: This trend thrives on partnerships between financial institutions and fintech companies. Banks provide the financial expertise and infrastructure, while fintechs contribute their technological innovation.

Image via Bain & Company

Embedded Finance vs Banking as a Service (BaaS)

While sometimes confused, embedded finance and BaaS are distinct concepts. Here’s a breakdown of the key differences:

- Customization: Embedded finance offers a high degree of customization, allowing businesses to integrate financial services seamlessly into their brand identity and user experience. BaaS, on the other hand, provides standardized financial services through APIs.

- Target Audience: Embedded finance targets the end-user, offering financial solutions embedded within non-financial products. BaaS caters to fintechs, digital banks, and other non-bank entities, providing the infrastructure to offer financial services.

- Monetization: Embedded finance utilizes a pay-for-use model, generating revenue based on the value delivered to the user. BaaS operates on a high-volume, low-margin model, profiting from the transaction volume facilitated through its platform.

The Future of Embedded Finance

Several trends are shaping the future of embedded finance in 2024:

- Rising Demand for Integrated Experiences: Consumers increasingly expect a seamless integration of financial services within the platforms they already use.

- Non-Bank Players Offering Financial Services: Tech giants and retail companies are actively exploring ways to offer financial products like loans and payments, blurring the lines between traditional finance and technology.

- Technological Advancements: Cloud computing, artificial intelligence, and APIs are making it easier to integrate financial services into a wider range of platforms.

The Road Ahead for Embedded Finance

Embedded finance presents a significant opportunity for businesses to enhance customer experience and unlock new revenue streams. Financial institutions must embrace digital transformation and collaborate with fintech companies to remain competitive in this evolving landscape. As embedded finance continues to grow, adaptability and a customer-centric approach will be paramount for success.